Did you know that high-value life insurance policies can offer more than just financial security? These hidden gems might actually be the secret to unlocking unforeseen benefits and financial strategies you never knew existed.

With the tumultuous economic changes affecting us globally, understanding the nuances of these life insurance policies has never been more crucial. This isn’t just about future-proofing your finances; it’s about making informed decisions right now.

In Thailand, life insurance is not just an investment but a cultural staple. High-value policies often go beyond simple death benefits, offering family legacies and business incentives. Many are surprised to learn that these policies can sometimes exceed the value of the insured’s own property holdings. But that’s not even the wildest part…

Meanwhile, in the USA, these policies are morphing swiftly to cater to modern needs. With tax advantages and even options for policy loans, it’s fascinating to observe how strategic these can be in estate planning. Many policyholders don’t realize the potential tax savings and investment opportunities hidden within. What’s even more surprising is the way these transformations are just beginning…

What happens next shocked even the experts. From innovative policy features to tax-deductible benefits, the intricacies of these high-value life insurance policies are about to rewrite the playbook. Stay with us as we uncover the secrets that could transform your financial future and legacy.

When it comes to high-value life insurance policies, Thailand’s offerings truly stand apart in their integration with cultural values and financial benefits. What’s lesser-known, however, is how these policies can leverage property acquisitions. Many policyholders use their benefits to acquire assets, assuring that wealth remains undiluted through generations. This concept aligns beautifully with Thai traditions of wealth retention. But top this with something more surprising—certain policies could even cover major medical emergencies completely.

As a policyholder in Thailand, understanding these benefits offers a significant advantage. These life insurance plans often come with built-in investment strategies and tax advantages that few other financial products provide. As such, they serve a dual purpose: providing a financial net and acting as an indirect investment tool. But why stop there? Some policies even allow for property investments, introducing a whole new dimension to wealth management.

Such financial strategies aren't only lucrative but also culturally resonant. In Thai society, securing family legacies is paramount. High-value life insurance aligns with this tradition, allowing cash-value accumulation that can be used or bequeathed strategically. This kind of asset-bundling isn’t just financially wise, it’s a gesture of love and foresight. Even more fascinating are the tax benefits attached, easing the pressure off heirs during claims. But what gets even more exciting is how these policies are being adapted to include coverage for imminent risks.

The question that boggles finance experts worldwide is, how far can these innovations go? It seems that these life insurance policies are not only here to provide security but also to redefine how wealth is perceived and managed in the modern Thai society. The melding of tradition with cutting-edge financial strategy fascinates. What you read next might change how you see this forever.

In the USA, high-value life insurance policies come with tax benefits that are often overlooked. Insiders understand that the cash-value component of permanent life insurance can grow tax-deferred, effectively allowing policyholders to build substantial wealth over time. Moreover, the death benefit, typically, is not included in federal taxable income, offering a significant advantage. But there’s a twist—did you know that policy loans can be tax-free?

These policies open new avenues for financial planning, especially in estate management. Business owners, in particular, find these policies beneficial, as they can leverage life insurance to cover inheritance taxes or even as a business succession strategy. This isn’t just about wealth preservation; it’s about utilizing multiple layers of financial tools, each maximizing the potential of future gains. Incredibly, some policies even offer clauses that protect against lawsuits, adding another layer of security.

Such advantages are crucial because they allow for greater flexibility in financial planning. Instead of bearing immediate tax burdens, policyholders can defer taxes, using dividend options or loan provisions strategically. The latitude to withdraw cash value for unplanned expenses or investment opportunities is an often under-utilized benefit. Insightfully, these provisions make life insurance a more dynamic and living asset than merely a static safety net. But wait, there’s yet another dimension to this strategy involving permanent life insurance—a savings tool like no other.

The possibilities here redefine conventional thinking about life insurance. These policies are proving to be exceptional tools for comprehensive financial planning. They offer adaptability and resilience against economic fluctuations, which is indispensable in today's volatile financial environment. Prepare to be astonished as we delve deeper into how these policies are changing the game for savvy investors.

Did you know that some celebrities use high-value life insurance policies not just as a safety net, but as a strategic financial tool? The way they structure these policies often mirrors complex estate planning with a focus on legacy and influence. In Hollywood, it’s not just about safeguarding tangible assets; oftentimes, it’s their brand that they’re insuring. Surprisingly, a few policies cover career-altering incidents such as scandals or accidents.

These policies are meticulously designed to ensure continued revenue streams and asset protection even after tumult. When musicians, for instance, insure their voices or athletes cover their limbs, high-value life insurance becomes a sophisticated form of hedging against losses that could impact their career irreversibly. The viability of such policies isn’t just in their protective features, but in their sheer adaptability to high-net-worth individuals’ unpredictable lifestyles.

It speaks volumes about the fluidity and power of life insurance policies in managing high-stakes careers. In the world of celebrities, everything can be monetized—even the intangibles. As their legacies often involve complex trusts and cross-border financial arrangements, integrating life insurance becomes a crucial element. It’s not only about sustaining wealth but also about maintaining influence and reputation. And you’d be shocked at the array of endorsements attached to such policies.

The striking part here is how accessible these strategies are becoming to non-celebrities. Leveraging life insurance for personal gain isn't just the domain of the elite anymore. What if regular policyholders could use similar strategies for maximum impact? It’s an intriguing prospect and one that’s increasingly within reach as these financial products evolve. Get ready to discover just how ordinary lives can emulate these extraordinary approaches in the coming sections.

When delving into the world of high-value life insurance, understanding the costs is crucial. It’s not just about premium payments; numerous hidden fees and charges can erode expected benefits. Surprisingly, many policies include management fees that increase over time—much like the notorious "creeping expenses" seen in other sectors. Policyholders may find that what was once affordable becomes cumbersome without vigilant management.

For potential policyholders, it’s essential to read the fine print. Actuarial costs, investment management fees, and administrative charges can significantly affect the net value of a policy over time. Knowing these factors ahead of time can empower consumers to make informed decisions aligned with their financial goals. Even more eye-opening are certain clauses that can virtually siphon value without the account holder’s knowledge.

Transparency is key, yet many policies are crafted in complex jargon, deterring a thorough comprehension of financial commitments. Some contracts are superficially attractive yet laden with conditions that could stifle financial stability. This makes it vital to engage with experts who can demystify these documents, providing clarity and perspective. But the story doesn’t end here; diving deeper reveals unexpected options that could alleviate some of these cost burdens.

Undoubtedly, understanding these elements allows buyers to truly harness the power of their policies. While costs can be a hurdle, the opportunity lies in utilizing insider knowledge to dodge pitfalls. The following sections will guide you through practical advice and reveal unheard-of techniques that experts use to maximize benefits, even in the face of hidden costs.

Policy loans are a lesser-known feature of high-value life insurance that offers surprisingly versatile applications. Unlike traditional loans, they don’t require repayments on a set schedule, giving policyholders remarkable financial freedom. What many don’t realize, however, is how these loans can effectively serve as emergency funds or strategically timed investments, often with little to no tax implications.

With interest rates on traditional loans climbing, leveraging policy loans can be an intelligent alternative. Accessing the cash value accumulated in life insurance can be quicker and less complex than securing a bank loan, offering a nimble financial resource. Even more surprisingly, those who use this strategy can avoid tapping into savings or liquidating investments, giving them a deft hold on their financial portfolio.

However, the benefits go beyond mere convenience. Calculating these loans into a larger strategic financial plan could mean significant savings and effective resource allocation. This financial flexibility is an attractive feature, especially for those looking to augment their investment strategies without immediately incurring expenses. But the unexpected twist is how these loans can support charitable giving, effectively stretching a policy’s impact far beyond personal gain.

Incorporating policy loans into philanthropic efforts can provide dual benefits: supporting causes close to one's heart and offering personal tax incentives. This kind of strategic thinking showcases the innovative ways high-value life insurance policies can transform traditional concepts of wealth management. Prepare to be astonished as we explore even more unconventional uses in upcoming pages, highlighting adaptive strategies suited for today's dynamic financial landscape.

The decision between whole and term life insurance policies is pivotal, yet often riddled with confusion. Whole life policies, although more expensive, offer long-term benefits, including cash-value accumulation. The predictability and forced savings mechanism appeal to disciplined savers. However, many are surprised at how term policies can still offer robust financial coverage without the hefty cost footprint.

It’s critical to recognize how term policies can be beneficial for specific financial objectives, especially when considering high-value coverages. For those seeking temporary financial protection, especially in providing for dependents in the event of an unexpected loss, term life delivers immense value. But then, there are nuances like the convertibility option—transforming a term policy into a whole-life policy without undergoing a new underwriting process that's enlightening.

Such options make term policies surprisingly flexible, especially for those wanting a phased approach to life insurance. They can begin with a lower-cost entry and evolve into more comprehensive coverage as life unfolds and financial capacities grow. While the allure of cash value is absent in term life, the affordability and adaptability make it a worthy consideration. As your financial situation evolves, understanding these distinctions becomes more imperative than ever.

Your choice hinges on your long-term financial goals, current budget, and understanding of benefits unique to each type. As you evaluate these options, it’s essential to align your choices with not only present circumstances but also future aspirations. What's more, this decision can influence generational financial planning in ways you might not have considered. The coming pages will deeper insights into how these decisions impact wealth strategy long-term.

Global economic shifts have noticeably influenced the features of high-value life insurance policies. Inflationary pressures have encouraged policy providers to innovate more adaptable and flexible products. Features today might include adjustable premiums or even inflation protection riders—a significant shift from the rigid terms traditionally offered. But what continues to astonish is the rapid evolution towards environmental and socially responsible policy options.

The growing awareness around climate change and sustainability has bled into financial products, including life insurance. Policyholders now have options to select investments linked with sustainable companies, promoting ethical wealth growth. The financial world’s move towards more responsible investing reflects a broader cultural shift that's marrying social consciousness with investment strategies. This evolution is reshaping not just life insurance but broader financial strategies globally.

This level of customization and adaptability is what sets apart modern-day policies from their predecessors. For the environmentally conscious consumer, life insurance that aligns with personal values represents a step forward, integrating social capital into financial growth. It encourages brand loyalty while leveraging financial products for a more significant purpose. But what really changes the landscape here is the potential for these options to set new industry standards.

These emergent trends are not only adding layers of choice but also pushing consumers to rethink how policies fit into their larger financial objectives. As high-value policies evolve with these influences, they continue to redefine what we consider valuable in a policy. We’re entering new territory where financial products are extensions of personal identity and belief systems, promising even more dynamic changes on the horizon.

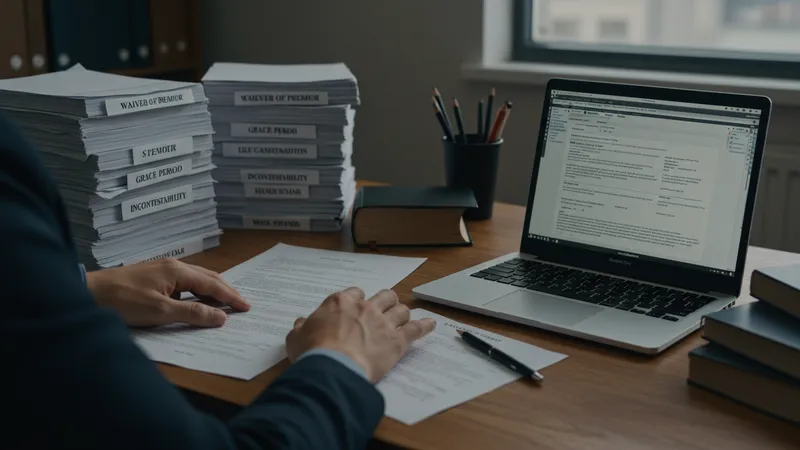

The language used in life insurance policies can be myhopically complex, often alienating those who are unaccustomed to financial speak. Policyholders need to wade through layers of legal jargon to grasp what’s being offered. But what remains elusive to many is how easily these terms can obscure potential pitfalls, reinforcing the necessity of expert consultation.

Deciphering terms such as "waiver of premium", "grace period", and "incontestability clause", to name a few, can turn the policy into an understandable, strategic instrument. These provisions might sound trivial, yet their implications during unexpected scenarios can be game-changing. For instance, a waiver of premium during disability can preserve the policy’s validity without financial drain.

Understanding these clauses becomes pivotal, especially when tailoring coverage to fit precise needs, and knowing what each exclusion truly entails. Terms that seem innocuous can potentially limit policy claims or affect payout during crucial times. It’s not just the comprehension that matters but also how one navigates these complexities to ensure safeguarded interests.

For potential policyholders, this knowledge liberates them from reliance on sales pitches and equips them with the tools for truly informed decisions. The good news is that there are resources available to help clarify and navigate these somewhat cryptic insights. The upcoming pages will offer tips on accessing expertise and efficiently breaking down these complexities for practical application in personal and business contexts.

The landscape of life insurance is on the brink of revolutionary transformation. Technology and digitalization are at the forefront, streamlining application processes and customizing policies with unparalleled precision. Instant underwriting, predictive analytics, and personalized digital dashboards present a future where policies are hyper-tailored to individual needs in real-time. But what’s utterly transforming is the rise of insurtech companies challenging traditional providers.

These insurtech enterprises are rewriting the playbook, offering digital-first, customer-centric experiences. From AI-powered chatbots providing 24/7 support to blockchain technologies securing user data and transactions, the efficiency gains are undeniable. This pivot towards technology doesn’t just enhance customer experience; it significantly lowers costs, presenting a more democratized form of access to comprehensive financial products.

Adapting to this new environment is essential for both consumers and traditional insurers keen on maintaining market relevance. The expectation is towards transparent, rapid, and seamless service—a far cry from prolonged paperwork and opaque fee structures of the past. The result? A clientele that’s not only more informed but more engaged with their insurance products than ever before.

The insurance industry’s digital future isn't just hypothetical—it’s impending and transformative. As the following sections will highlight, the coming innovations seek to redefine not only the shape of policies but also the manner in which they integrate across financial ecosystems. It’s an evolution that beckons you to reconsider the role life insurance plays in broader asset management and personal planning.

Industry experts have had their eyes opened to the bountiful opportunities that high-value life insurance policies present, particularly in untapped markets. The next generation of policyholders is more discerning and informed than previously, and insurers are responding with increasingly sophisticated products. Trend analysts predict a growing demand for transparent and socially responsible offerings, aligning with broader market preferences.

Among the discussions, a common theme emerges: policyholder engagement. The next frontier isn’t just about adding new features but fostering genuine engagement. Imagine interactive policy management systems where users can tweak coverages in real-time based on lifestyle changes. Experts foresee this trend as integral for maintaining loyalty in an era where consumers are spoiled for choice.

The persuasive need to adapt to consumers' evolving demands means insuring more than just income and property—it’s about safeguarding lifestyles. Financial products that enhance or support wellbeing, incorporating elements like wellness benefits or preferential rates, stand to redefine traditional concepts of insurance. Analysts are closely monitoring these shifts, predicting even more impactful synergies between life insurance and digital health metrics.

As these innovative features gain popularity, the lines between insurance, investment, and lifestyle services will blur, forming comprehensive, personalized solutions. This evolution is more than just a trend—it’s a shift toward holistic financial stewardship, allowing policyholders to enjoy life while being prudently prepared for future contingencies. With multiple industries overlapping, the synergies promise to usher in a truly unique era for how high-value life insurance policies are conceived and executed.

The modern workforce is changing rapidly, with more contractors, freelancers, and gig workers demanding unique solutions. Standard life insurance policies often fall short of meeting these new requirements. Recognizing this gap, insurers are becoming more agile, adapting policies that reflect changing work realities and support flexible income patterns.

For those in non-traditional employment, customized coverage options offer a means to secure financial protections previously unavailable. These aren't just responses to trends; they are proactive adaptations that position insurers as allies to the gig economy. An adjustable policy with income fluctuation riders, for instance, provides coverage security even amid inconsistent revenue streams.

This kind of flexibility has gained traction, seen especially in the uptake of life insurance bundles tailored specifically for freelancers. Such arrangements not only provide peace of mind but bolster workers' capacities to focus on their careers without being distracted by financial uncertainties. Furthermore, experts suggest the integration of benefits like skill enhancement or project insurance for specific gig assignments could be revolutionary.

Such evolution in policy structure echoes wider economic shifts, fostering a stable backdrop against which the new workforce can thrive. Embracing these offerings prepares individuals and families for financial variability in more adaptable, resilient ways, mirroring the fluid nature of today’s career paths. As the employment landscape continues its metamorphosis, its influence on life insurance will only expand further, challenging insurers to keep pace with innovation.

Looking back, policyholders often reveal insightful lessons gained from navigating the complexities of high-value life insurance. One recurring sentiment is wishing they'd understood policy flexibility earlier. Many were unaware of upgrade options or amendments that allow adjustments to match life changes. This knowledge could make a significant difference in leveraging policies to their fullest.

Questions around additional riders—options such as accidental death or critical illness cover—are prevalent. Too often, policyholders discover post-purchase that meaningful additions are available, offering greater protection or tailored solutions to individual needs. These missed opportunities for optimization stem from a lack of proactive exploration or robust advisement by insurers.

Moreover, the value of professional advice can't be overstated. Access to knowledgeable counsel during purchasing, rather than post-issue, serves clients better than reactive measures. Indeed, a consistent theme is the benefit derived from investing time with financial advisors to demystify conditions and optimize asset reinstatement when needed. Experts corroborate these experiences, indicating significant growth in demand for transparent policy planning.

As life circumstances and goals change, these insights should compel policyholders to reassess current plans periodically. With options emerging continually, early insights into possible adjustments could foster an all-encompassing financial strategy. The profound realization for many is that staying informed and engaged with policy developments dramatically enriches one’s financial toolkit. This revelation can redefine financial planning and security for generations.

Education plays a decisive role in the decision-making process for high-value life insurance. A well-informed consumer can leverage knowledge into negotiating better terms or acquiring added features. While many view insurance as complex, accessible information has begun leveling the playing field, enabling greater transparency across the board.

Initiatives that focus on insurance literacy are gaining momentum, aided largely by digital educational platforms offering workshops, tutorials, and guidance in easily digestible formats. The result is not just a financially literate populace but one that demands clarity and innovation from their insurers. The positive effects are being echoed throughout the industry, challenging providers to redefine offerings continually.

However, gaps persist, emphasizing the need for ongoing awareness campaigns. Compelling statistics reveal an informed policyholder is likelier to renew or expand coverage, a fact not lost on thoughtful insurers. Armed with comprehensive insight, consumers are empowered to make precise, data-driven choices that reflect their genuine financial needs and horizons.

Consequently, the marketplace for high-value life insurance grows ever more competitive. Education emerges as a linchpin in cultivating a savvy consumer base, leading to better product customization and satisfaction. As these initiatives evolve, unsurprisingly, industry's trajectory toward increased transparency and customer-centric innovation becomes clear, and the era of consumer empowerment in financial products draws nearer.

Undervaluing the potential of high-value life insurance policies is a common pitfall that can erode financial stability over time. Misunderstandings surrounding policy potential and benefits might cause individuals to miss out on substantial tax advantages or investment opportunities. Such oversight stems from a lack of comprehension rather than the policy’s deficit.

Moreover, an undervalued policy could lead individuals to perceive it solely as a precautionary tool, rather than an active component of a broader financial strategy. Risk factors tied to ignoring policy enhancements or the failure to leverage it as a wealth-building vehicle can lead to missed opportunities. Such misconceptions highlight the critical nature of ongoing policy evaluation and awareness.

Additionally, policy devaluation may result in individuals compromising on coverage, relinquishing vital financial security they could otherwise afford. Protecting against this requires a proactive approach to policy management, actively seeking out updates and innovations to capitalize on every available opportunity. The challenge lies in continuously reminding oneself of policy longevity and growth capacity.

The future of financial planning depends on heightened awareness of policy value. Reflection and recalibration of one’s current standing against potential upgrades or alternate strategies reinforce life insurance as an asset, rather than merely an expense. Such consideration ensures policyholders are well-positioned to navigate life’s uncertainties, coalescing security with strategic growth imperatives.

And just like that—counting every permutation and psychological trick employed—we've scratched only the surface of what high-value life insurance policies can offer. The potential they unleash upon discovery can reinvent words like "security" and "investment". When carefully evaluated and adapted, these policies can secure legacies and even alter family fortunes.

But this world of lucrative possibilities demands a discerning eye. As you journey through your own financial gameplan, the lessons here can fortify that future. Share this insightful exploration with others on these uncharted waters, for the secrets learned here promise empowerment—not just wealth, but foresight to endure the test of time.